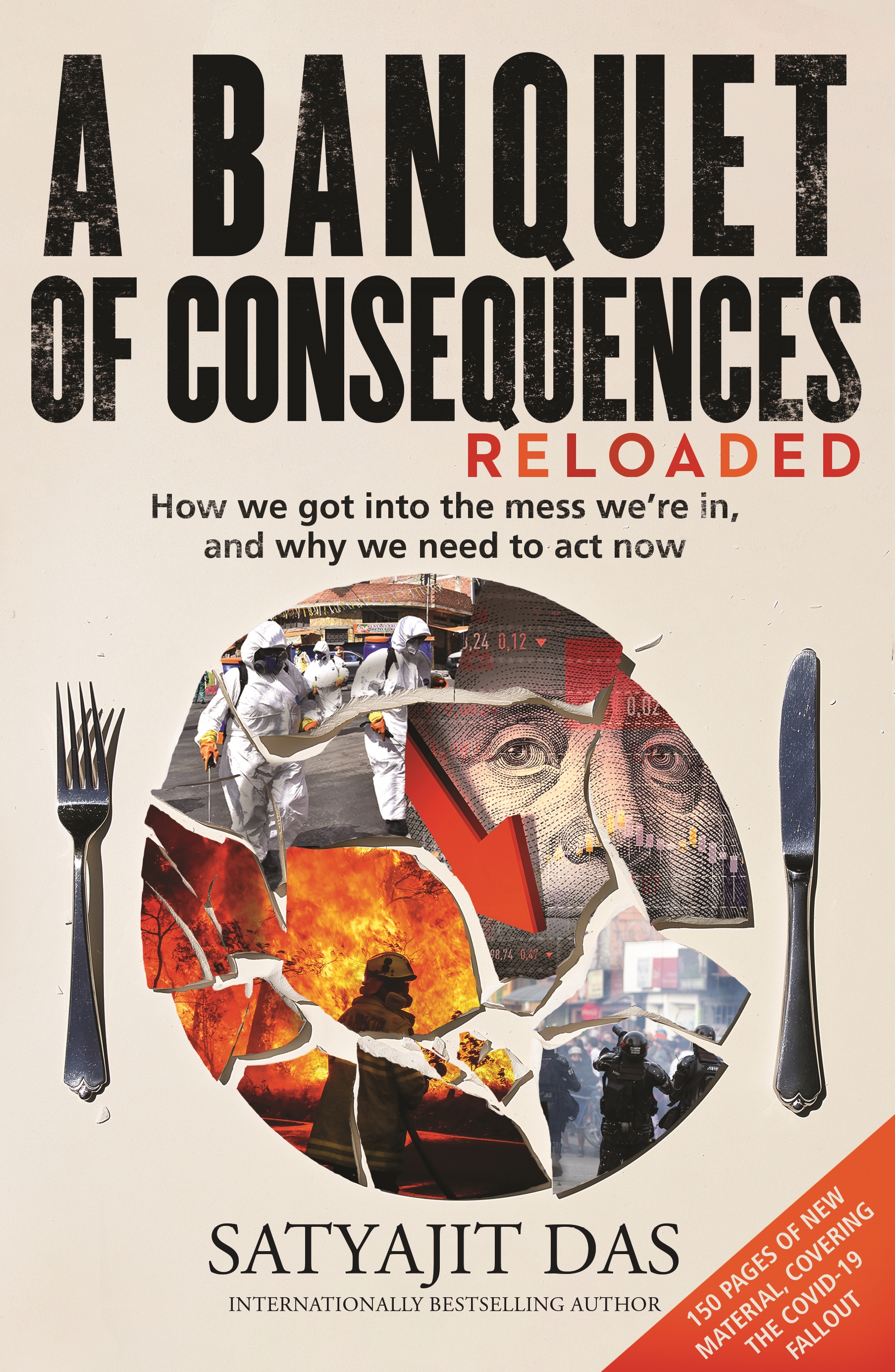

In A Banquet of Consequences Reloaded we get the world view of an apostate investment banker, and a very grim weltanschauung it is. Essentially, Das argues that the modern economy is long overdue for a massive correction and that debt-fuelled growth cannot continue. ‘Living standards will decline in real terms. Citizens will have to save more and consume less. Working lives will lengthen … Financial institutions need to return to their actual role of supporting economic activity rather than engaging in or facilitating speculation.’

To justify this cheerful prognostication Das reviews economic world history since World War II and seeks to show that the GFC was the inevitable consequence of the ‘Goldilocks’ economic policies of the 1990s and that what we are now facing is a period of indefinite stagnation. In a lengthy postscript he considers events since 2015 and sees the pandemic as administering the coup de grace to financial capitalism. ‘The pandemic showed that the human race may have spun out the clock as long as it can … the rate of change will overwhelm attempts at containment and mitigation.’

In case the reader is in any doubt as to what this means Das then quotes from the parable of the Wise and Foolish Builders in the Gospel of Matthew. ‘… and great was the fall thereof’.

If only. I get to tell you folks that the zero-sum prognostications of economists have been terrifying children since the days of Ricardo and Marx.

The problem with economic theory in general, and A Banquet of Consequences Reloaded in particular, is not that they are not genuine attempts to improve our world. Das indeed makes many sensible points about the egregious nature of financial speculation using derivatives and the climate emergency and the baleful consequences of economic inequality. Nor is it that (the right kind of) economic theory is not useful. The reason our economy is (for now) strongly recovering is precisely because the ghost of Keynes again walks the corridors of Treasury.

Rather the problem is that much economic reasoning is a priori and driven by models which, while they work perfectly on paper, have limited relationship to reality. The basic premise of the book is that debt levels are unsustainable, and that scarcity will dominate future economic conditions. That proposition however is simply not borne out by what is happening in reality. Indeed, Modern Monetary theory advances the startling proposition that countries with a sovereign currency can indefinitely fund government spending by bond financing at least until capacity constraints start to generate inflation. The problem is not debt, its capacity to produce goods and services. And if you think I made that up check out The Debt Delusion by John F Weeks. And if you are still sceptical consider the economies of the US and Japan which have essentially been run on massive government deficits for the last 30 years without a squeak of inflation.

But I think he misdiagnoses the problem. They call economics the dismal science for a reason.

Reviewed by Grant Hansen

0 Comments